2024 Forex Market Insights

Read Time: 8 Minutes

Throughout the year of 2024, we’ve observed some significant economic shifts and global events that have influenced market movements in their own way. Central bank policies were front and centre, with the Federal Reserve, European Central Bank, and Bank of Japan steering market sentiment through interest rate decisions and inflation management.

Geopolitical events further intensified market volatility, from the U.S. presidential election to regional conflicts and global trade renegotiations. These developments highlighted the forex market's sensitivity to political transitions and international agreements – providing some great trading opportunities along the way, on the back of the resulting volatility.

There were talks of central bank digital currencies (CBDCs) and the integration of AI-driven trading tools, which brought us both opportunities and challenges, fundamentally altering how traders approach the market.

Economic indicators like inflation trends, employment data, and GDP growth provided critical insights into currency dynamics, while liquidity patterns and institutional trading flows shaped the forex market 2024 behaviour.

- Central Banks & Economic Indicators

- Geopolitical Influencers

- Forex Market 2024 – Behaviour Analysis

- A Technical Recap

- Conclusion – Lessons From 2024

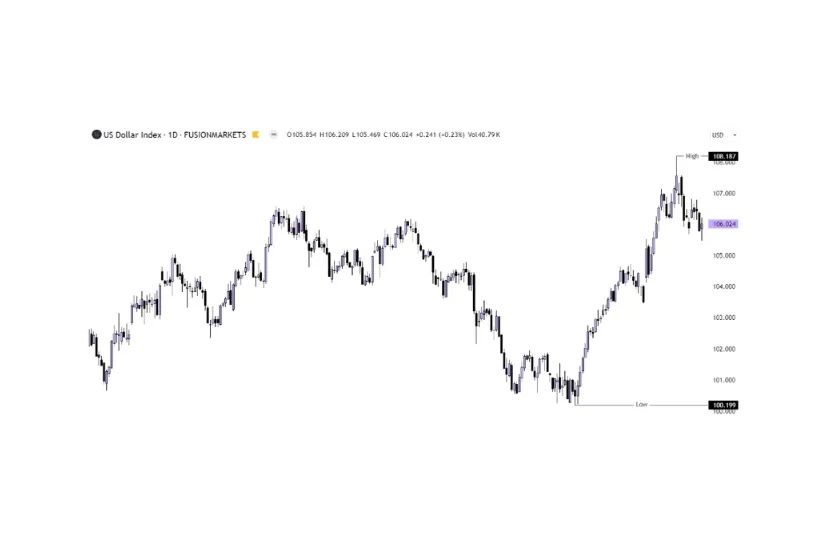

Economic indicators continued to determine forex market 2024 movements. Inflation trends, employment data, and GDP growth became focus points for traders in their market analysis. However, central banks were the driving forces behind many of 2024’s forex movements. One of the key influencers being the Federal Reserve (FED), which continued to balance inflation management with economic growth. Its policy decisions caused notable fluctuations in the dollar index.

In Europe, the European Central Bank (ECB) adopted a measured approach, focusing on stabilising the eurozone whilst observing varying economic growth rates. Its quantitative easing measures influenced liquidity trends and regional currency movements.

Across the Atlantic, the Bank of England faced challenges as the UK’s post-Brexit economy dealt with a persistent level of inflation.

The Bank of Japan remained committed to ultra-loose monetary policies, maintaining pressure on the yen – of which was a prime contender in the carry-trade space. Meanwhile, several emerging economies grappled with inflationary spikes, prompting central banks in countries such as Brazil and India to tighten policies.

Inflation remained a dominant theme, with central banks in developed and emerging markets adjusting their policies to manage rising prices. The U.S. inflation rate, in particular, was a critical driver of Fed decisions, indirectly shaping the dollar's global standing.

Whilst the U.S. demonstrated moderate growth, China’s slower-than-expected recovery impacted commodity-linked currencies like AUD and CAD. In addition, trade balance data highlighted the fragile state of international trade, further complicating currency dynamics.

One of the year's most impactful events was the U.S. presidential election, which drove volatility across global markets. Policy discussions on trade agreements and economic reforms led to fluctuations in the USD, particularly against currencies like the euro and yen. With President Donald Trump still in the process of taking office, we can expect to see further geopolitical developments and forex price movements as we head into 2025.

Regional conflicts and political transitions also applied pressure on currencies. A key one being the tensions in Eastern Europe which influenced the euro's trajectory, whilst political instability in the Middle East affected oil-exporting nations' currencies such as the Russian Ruble and Canadian Dollar. In addition to this, trade agreements, such as renegotiations between key Asia-Pacific economies, created ripple effects in commodity-linked currencies like the Australian and Canadian dollars.

The forex market 2024 exhibited unique behavioural trends, characterised by pronounced volatility and evolving liquidity patterns. Traders observed spikes in volatility following key central bank announcements and geopolitical events, which created both challenges and opportunities.

Liquidity trends shifted significantly, with institutional trading flows dominating high-volume trading periods. Cross-border capital movements also surged, driven by divergent economic recoveries among regions. For instance, the U.S. attracted significant foreign investment due to its relatively stable economic outlook, bolstering the dollar’s strength against other major currencies.

Technological advancements further influenced market behaviour. AI-driven trading platforms improved trade execution efficiency, while blockchain technology introduced greater transparency in cross-border transactions. The digital currency evolution has added another layer of complexity, as traders adapted to the increasing integration of CBDCs into mainstream markets.

These behavioural insights reveal the dynamic nature of the forex market in 2024, emphasising the need for traders to remain agile and leverage advanced tools for navigating this ever-changing landscape.

In addition to observing the fundamental influencers of 2024, we can put it all into context by observing the daily chart for the year.

DXY

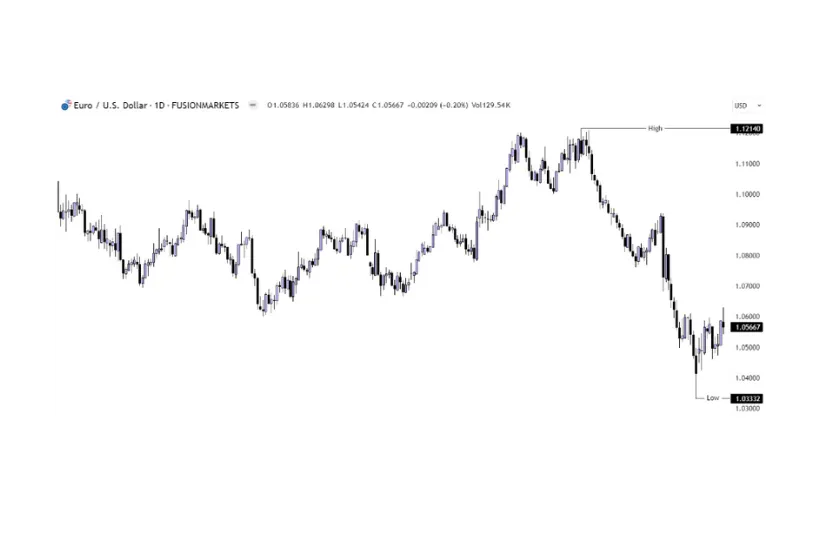

EURUSD

As expected, the US Dollar movements were inversely correlated with the EURUSD reaching a high of 1.12140 and a low of 1.03332.

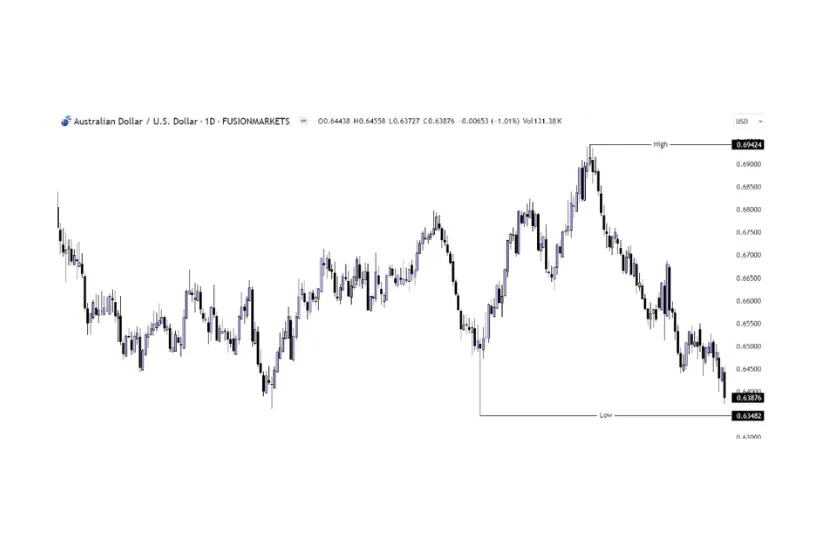

AUD & NZD

Our Aussie dollar has provided some fantastic trading opportunities this year – with range-bound strategies taking advantage of Q1 & Q2, before trend-following strategies amplified those returns with the increased volatility in Q3 & Q4, resulting in a high of 0.69424 for the year, and a low of 0.63482.

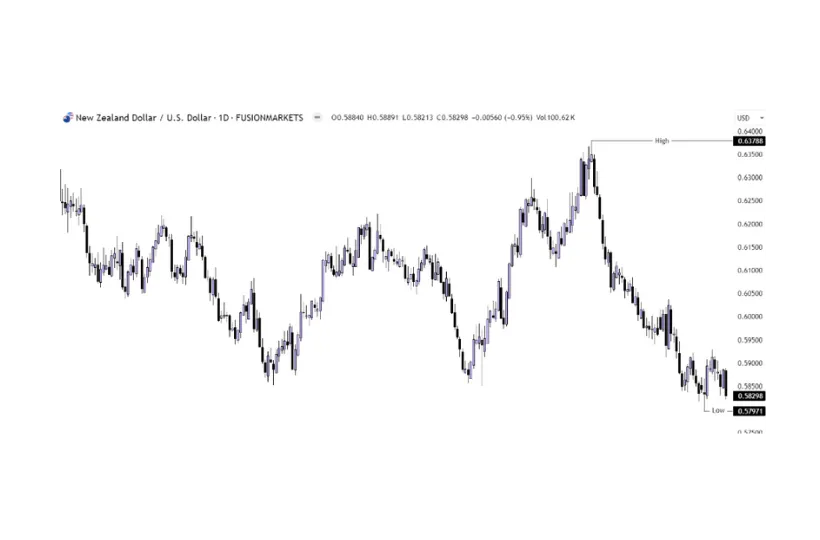

Across the ditch, the Kiwi Dollar has performed very similarly, with a high of 0.63788 and low of 0.57971.

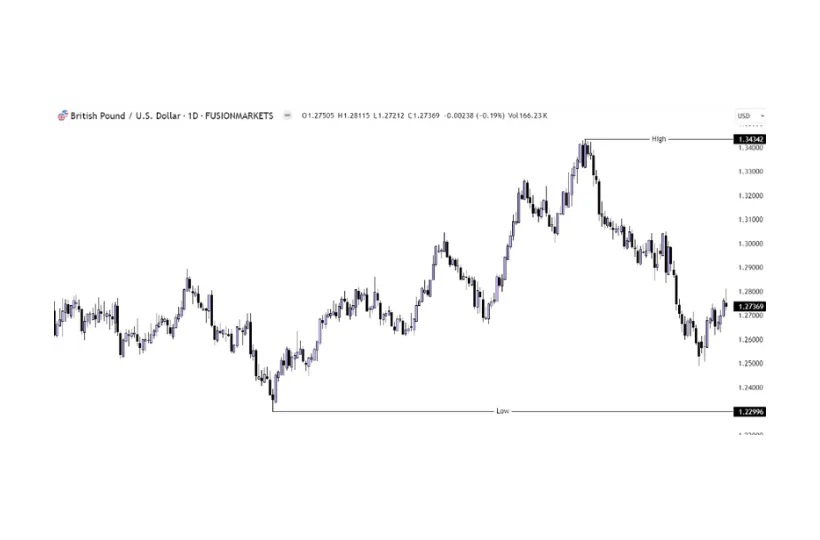

GBP

The trend was your friend for the GBP this year – providing a long-term bullish trend, before reversing to a now-downward trend. A prior low for the year at 1.22996 was met with a resulting high of 1.34342 at the conclusion of the bullish trend.

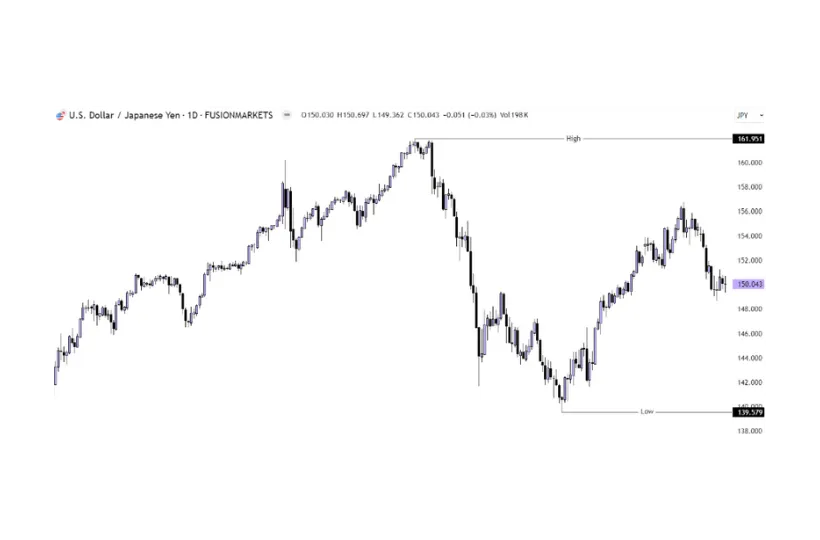

CHF & JPY

Love it or hate it, the Swiss Franc was a trend traders’ dream this year, with a bullish trend providing a high of 0.92244, followed by a resulting down trend reaching a low of 0.83744.

We all know the story with the Yen this year, including multiple instances of intervention by the BoJ. Whether you’re taking advantage of the carry trade, or simply riding the trend, we saw textbook trending reaching a high of 161.951 and a low of 139.579 for the year.

The 2024 forex market has been a year of developments, from central bank policies, economic indicators, geopolitical events, to technological advancements...

Disclaimer: Economic conditions are complex and rapidly evolving. This overview provides an educational perspective based on available information as of late 2024.

We’ll never share your email with third-parties. Opt-out anytime.

How Global Interest Rate Divergence Is Shaping Forex Opportunities in 2025