Preview: US April CPI 12 May 2026

Read Time: 4-5 minutes

The US April CPI report drops on Tuesday, and it's the major data event of the week.

This will be the first clean month-on-month look at how the energy shock from the Iran conflict is filtering through to headline inflation.

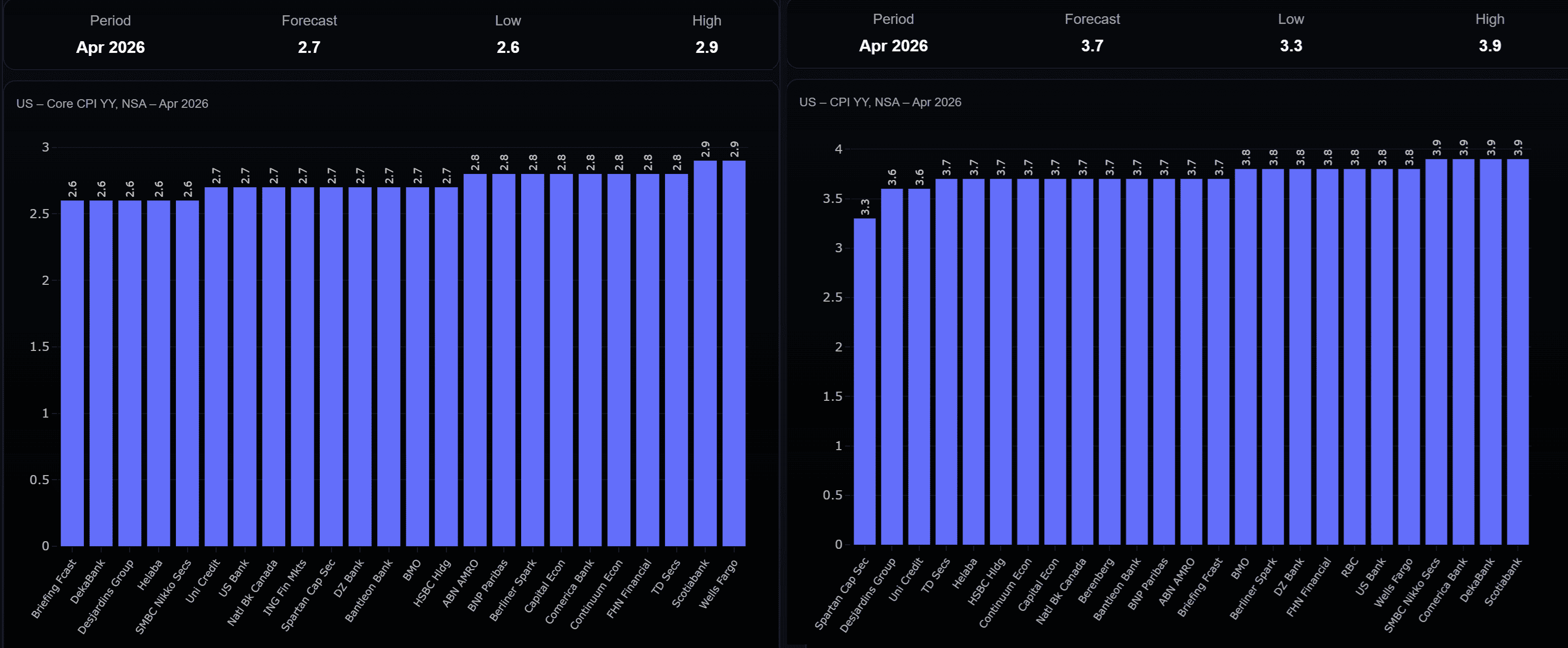

Markets are forecasting headline CPI to rise 0.6% MM, easing from the hot 0.9% print in March.

That would lift the annual rate from 3.3% to around 3.7%, which would mark the highest annual rate in nearly two years.

Core CPI is expected to rise 0.4% MM, a touch firmer than the 0.2% seen in March, with the annual rate seen nudging higher to 2.7%.

However, some one-off upsides have been backed into the Core number related to rent index adjustments, so any upside in Core coming from rent could be discounted.

Looking at the forecast distributions above, it’s worth noting that the minimum estimate on the headline is out outlier, and means any print below 3.6% can already offer a decent surprise.

There are a few moving parts that make this print messier than usual.

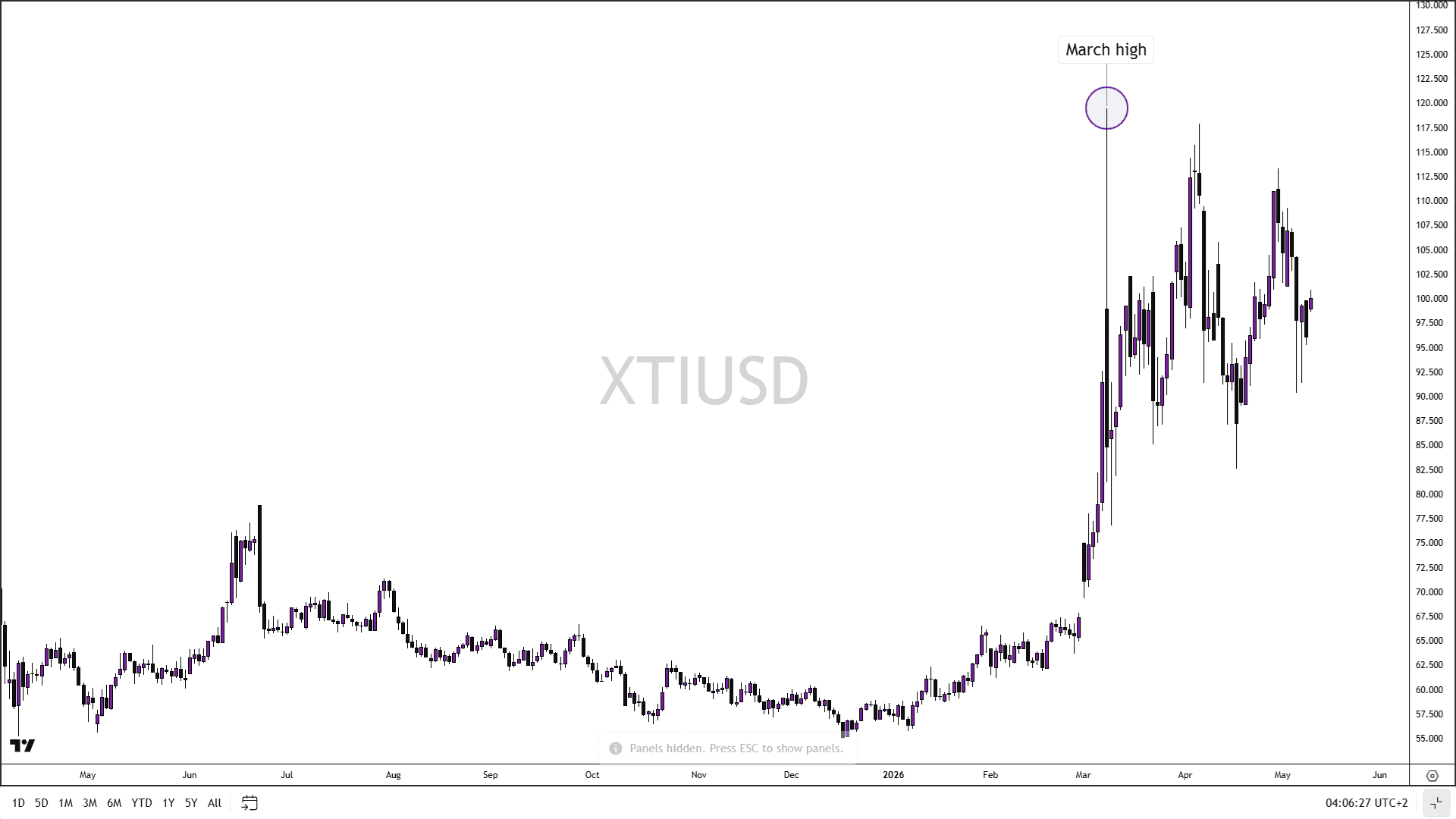

The lag between crude prices and prices at the pump means April readings can still capture some of the March spike in oil.

Higher jet fuel costs are also expected to feed into the core basket, with some estimates pointing to a 10–15% jump in airfares for April and May travel.

When the upside is driven by geopolitics that can whipsaw between extreme optimism to pessimism in a few minutes, the spike makes it a tricky one for policy makers to navigate.

We already saw Fed officials take a more patient stance at the April FOMC with three dissenters (Hammack, Kashkari and Logan) voting against including any easing bias in the statement.

There was also a shift in the statement around inflation, with the FOMC seeing inflation as 'elevated' instead of 'somewhat elevated”.

However, it’s unlikely that one print will materially shift the bank’s patient stance as long as the Middle East uncertainty remains.

There is a bit of a caveat to keep in mind about this week’s CPI.

For the headline number, a beat is arguably less market-moving than a miss.

When everyone already expects higher energy prices to push inflation higher, an acceleration is firmly baked into consensus forecasts.

A meaningful miss, on the other hand, would suggest the energy passthrough is more contained than feared, and that's the type of surprise that can move the dial.

For core, the asymmetry runs the other way.

With an obvious lag between headline and core, a hot core print would surprise markets more than a miss, as it would show risk that higher energy costs are already feeding through to broader prices much faster than expected.

Of course, a large surprise in either direction will still matter for rate pricing, but as usual, the cleanest directional moves come when headline and core tell the same story.

The cleanest setup for dollar bulls would arguably be both headline and core printing hotter-than-expected, ideally with RISK-OFF sentiment at the time.

The cleanest setup for dollar weakness or upside risk for US equities would be both prints missing estimates, with RISK-ON sentiment at the time.

The trickier scenario is a split print and will be difficult to navigate.

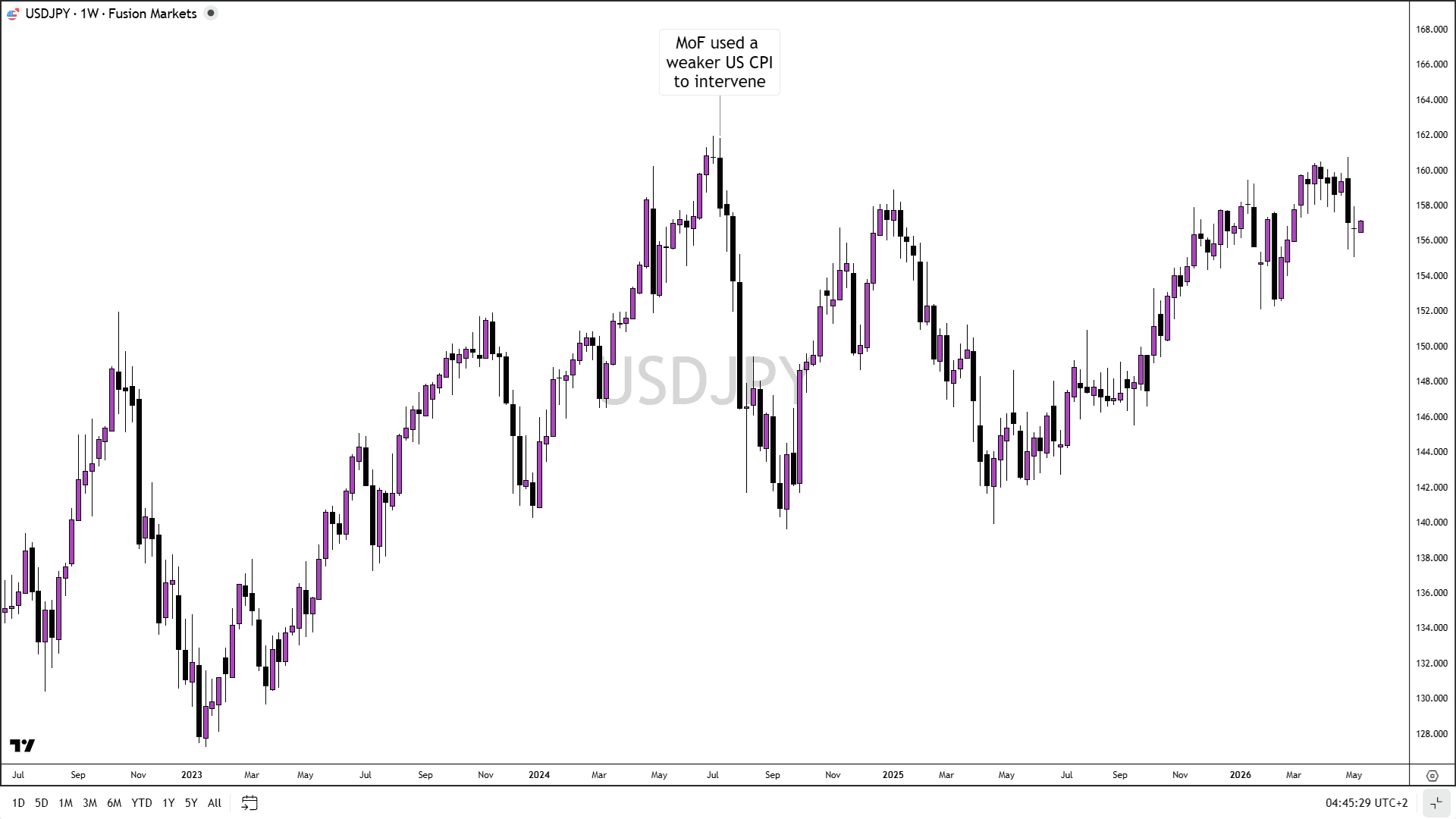

It’s also worth keeping JPY intervention risks in mind for this CPI print.

Recall in July 2024, the Japanese MoF tried to take advantage of a dollar-negative market event to prop up the JPY with intervention.

That strategy achieved a very decent result for the MoF as it saw markets unwind JPY shorts in a very short space of time.

With the two intervention attempts in the past two weeks, watching intervention risks around CPI will be important.

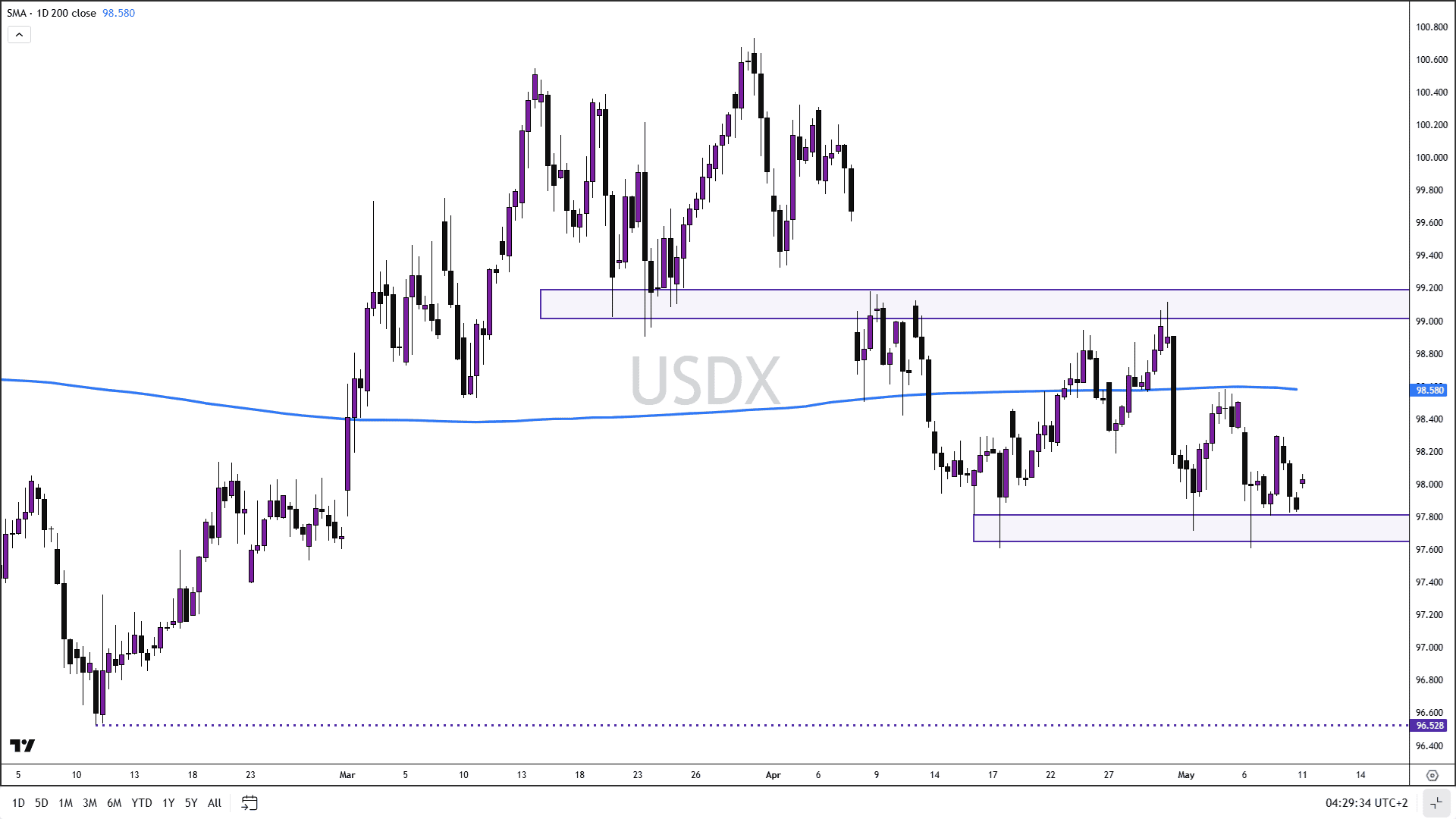

The dollar has held up relatively well despite recent peace optimism and the Japanese intervention in the yen.

Looking at key levels, there are two noticeable resistance areas for the Dollar, with the 200DMA close to 98.60, and then major structural resistance at 99.00.

A break above the 200DMA could put a test of structural resistance in play.

On the downside, the Dollar has survived multiple tests at key support around the 97.80 zone.

A break and close below that zone brings the February lows at 96.50 in focus.

We’ll never share your email with third-parties. Opt-out anytime.