Gold as an inflation hedge: Debunked

Read Time: 4-5 minutes

Has someone ever told you that gold is an inflation hedge?

Even though people treat this idea as financial common sense, the data tells a very different story.

Let's start with a number that should end the debate…

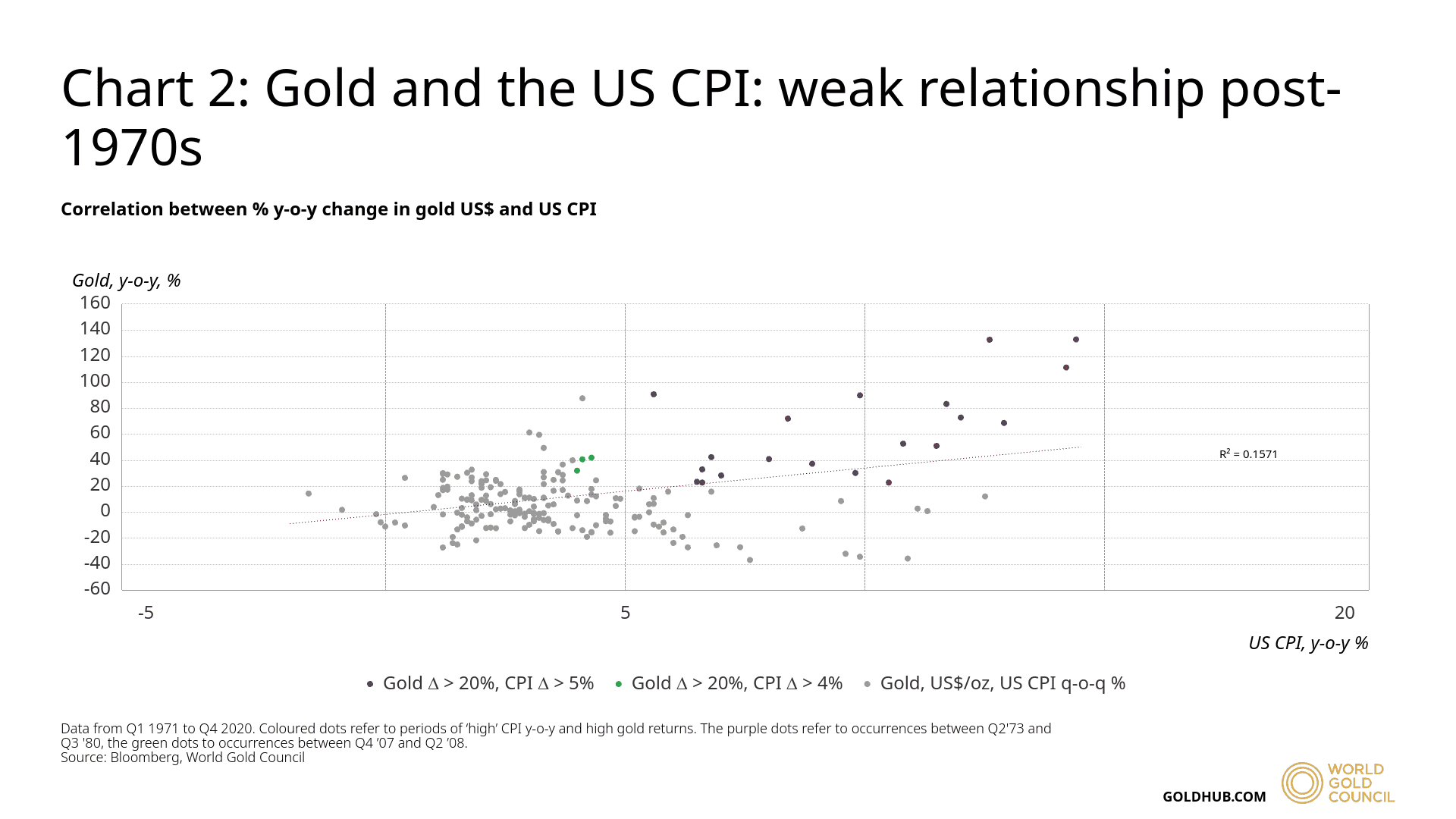

The World Gold Council published research showing that only 16% of gold's price movements since the 1970s can be explained by changes in inflation.

What about the remaining 84%? Well, it turns out that over the past 50 years, the bulk of gold’s price movements cannot be linked back to inflation at all.

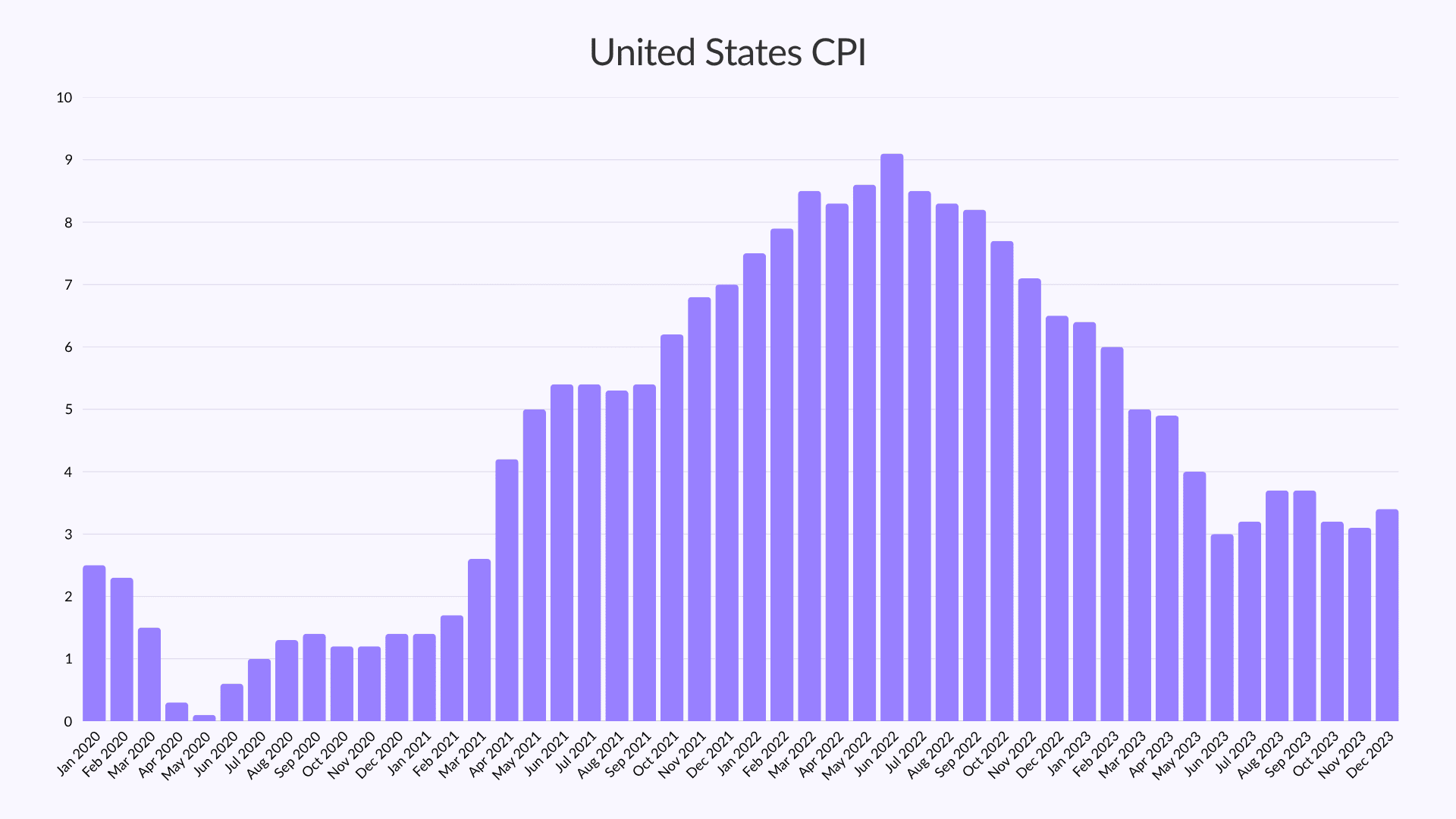

Let's look at the most recent real-world test. 2021 and 2022 were the worst inflation surges in forty years.

CPI climbed from below 2% to 9.1% in the US. Grocery prices, gas, rent, electricity, you name it, prices for almost everything went up sharply.

It was the most severe inflationary episode in a generation.

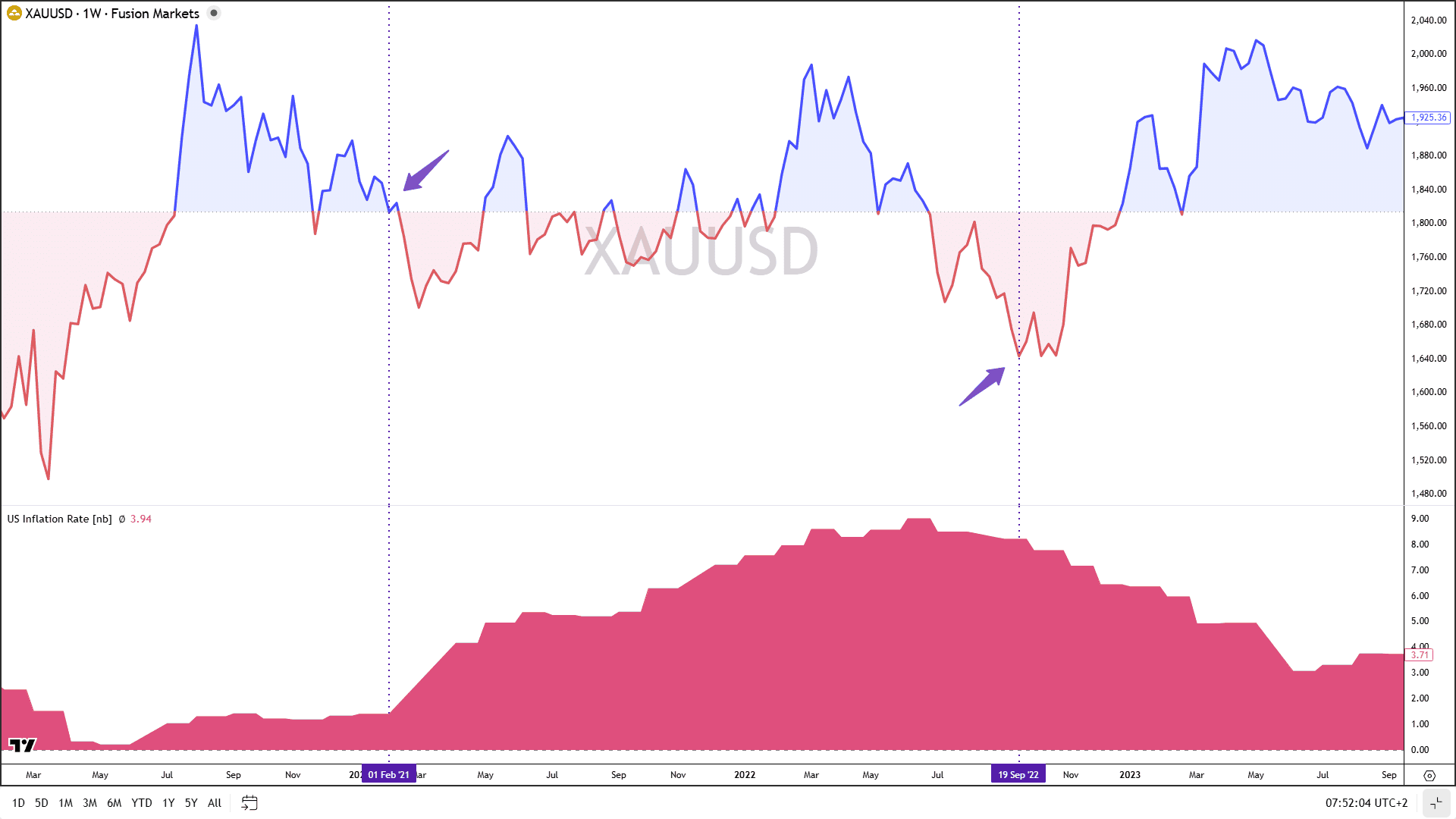

And what happened to gold during that time?

Surely if gold were an inflation hedge, then it must have been soaring during that time, right?

No. If you study that period, you’ll find no statistically significant price response in gold. Zero.

Instead, gold returns were mostly flat from the start to the peak of the 2022 inflation scare and only began to perform well when inflation began to fall.

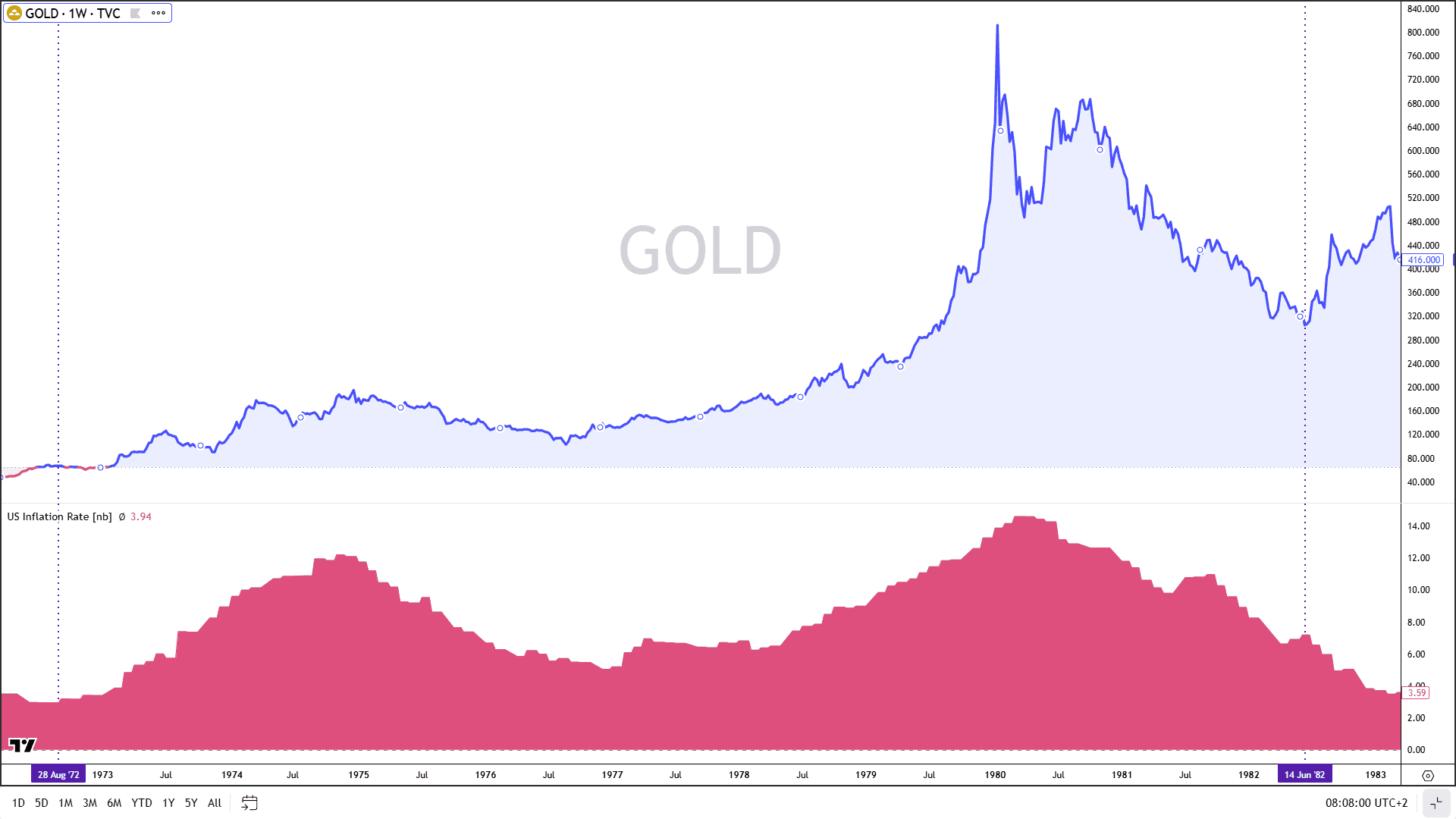

And 2022 isn’t the only example. Between 1980 and 2000, inflation averaged just over 4%, but gold peaked in 1980, and it took 27 years to regain those prior highs.

Now this is usually where the gold bug will jump in and start referencing the 1970’s.

And yes, in their defence, during the 70s there was a statistically significant relationship between gold and inflation.

Gold rose by over 2000% as US CPI ran up to 14%, but inflation wasn’t the cause.

In ’71, Nixon ended the gold standard, which broke the $35 fixed price cap that had suppressed gold since before the 2nd world war.

Then you had a suppressed market with price discovery, two brutal oil shocks, massive fiat debasement, and global geopolitical chaos.

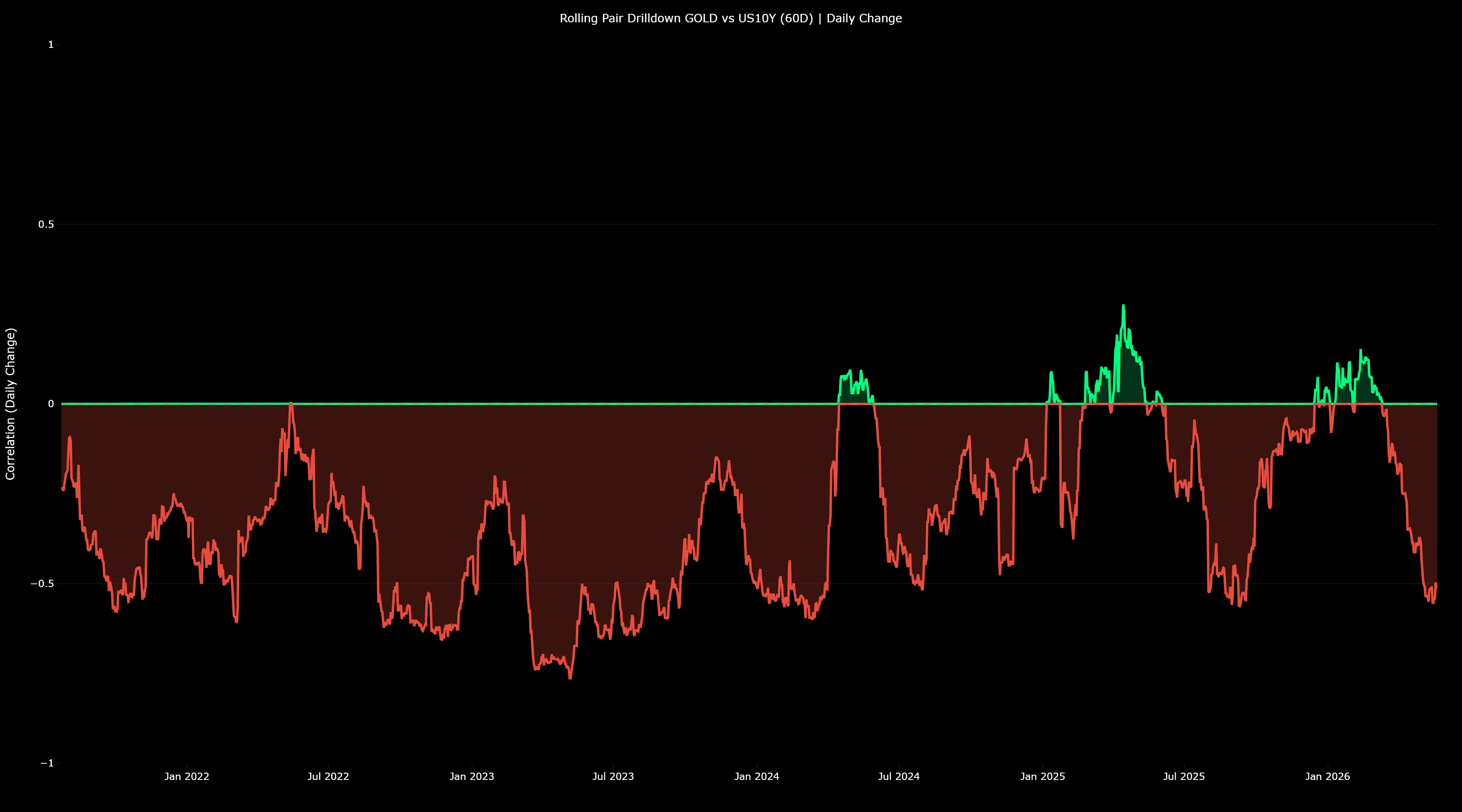

In other words, gold is a hedge against monetary debasement and falling real yields, but not against inflation

The more correlated drivers are usually real interest rates and the dollar.

When real rates are negative, or bonds pay less than inflation, gold is attractive.

But when the Fed hikes rates aggressively and real yields go positive, an asset like gold that has no yield and no dividend becomes expensive to hold.

But, if gold isn’t really a good inflation hedge, what is?

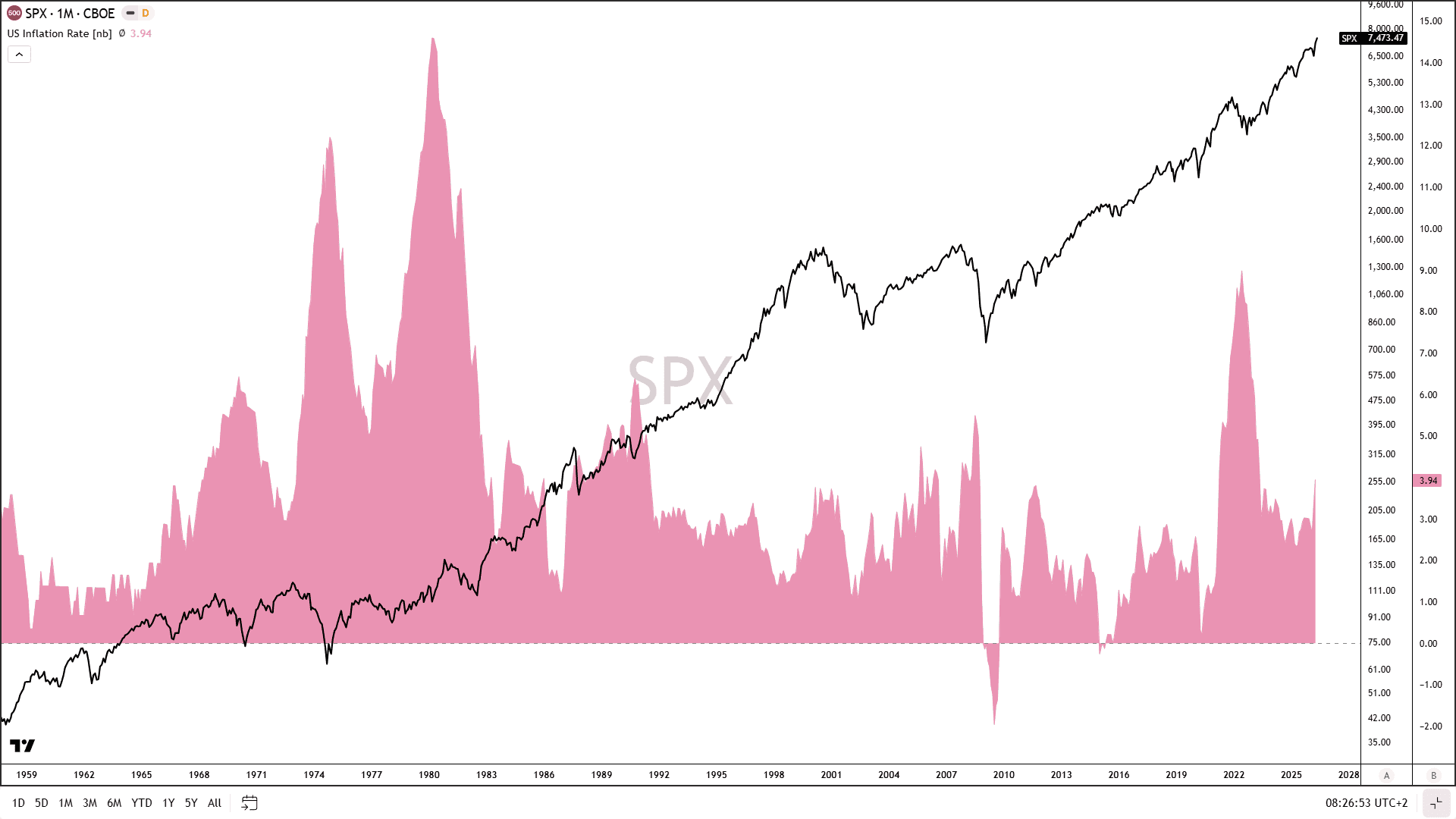

The data points to equities.

Since 1970, $10000 invested in the SPX has given a $2 million higher total return compared to gold over the same period.

And it’s important to remember that the outperformance has narrowed drastically due to gold’s historical 2026 surge.

This is also where opportunity cost is another important consideration. The time investors had to wait for gold to make it worth their return is why many institutional investors have preferred equity-heavy portfolios.

Yes, there are periods when equities can take eye-watering plunges, like in 2000, 2008, and 2022. However, in the long run, the long-term investor has been rewarded more by equities than by gold.

Does gold still have a place in a well-rounded portfolio?

The majority of asset managers would arguably say yes, as gold has proven itself to be a hedge against fiat debasement and global geopolitical chaos.

So, gold can have a place in a portfolio, but protecting against inflation isn’t it.

We’ll never share your email with third-parties. Opt-out anytime.